Sterling Exceeds Expectations in September

Tuesday 04 October 2016

The UK may have voted to leave the EU, but official figures for September did not reflect the immediate and significant economic impact that was predicted, writes Ben Scott.

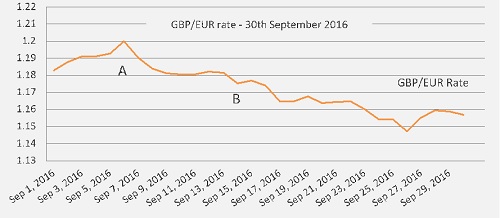

September saw a slow start to the month, with sterling boosted by a better-than-forecast Purchasing Managers' Index (PMI). Manufacturing and construction PMI data beat forecasts coming in at 53.3 and 49.2 respectively (PMI of 50 represents growth).

Although this was better than expected, this is not yet considered entirely positive.

Economic data is exceeding Brexit predictions, and it is still a possibility that the Bank of England will cut interest rates this year, which will support sterling as we approach year-end.

European confidence is the lowest it has been since March and the UK’s decision to divorce from the EU is undoubtedly a factor.

In Germany, retail sales figures were better than the forecast, which added some strength to the euro.

Post-Brexit, PMI was revised up to a composite of 53.6 from 47.6. PMI did start from a low base in August after the referendum result, but this remains the sharpest rise since November 2013 and the largest jump on record for services PMI.

Better than expected data saw GBP/USD test 1.3360. It settled back to 1.3345, but with EUR/GBP still looking soft, forecasts and figures are being watched with interest. August data from various sources indicated that the UK service sector returned to growth, but this came after a month of disruption attributed to the outcome of the EU referendum.

Abrupt contractions in output and new business in July were also linked to disruption related to the outcome of the EU referendum. But, the latest data suggests uncertainty has somewhat abated and the UK is returning to growth.

Moreover, the forward-looking business expectations index recovered most of the ground lost in July, when confidence took a knock amid political and economic uncertainty, although numbers remain weak by historical standards. The latest data also indicates rising inflationary pressure that is also linked to the weak pound.

The survey's headline figure is the seasonally adjusted Markit/CIPS UK Services Business Activity Index. This single-figure measure is designed to track changes in total UK services activity compared with one month previously.

"It remains too early to say whether August's upturn is a dead cat bounce [sudden recovery] or the start of a sustained post-shock recovery," said IHS Markit economist Chris Williamson. "But there's plenty of anecdotal evidence to indicate that the initial shock of the June vote has begun to dissipate."

On 15 September the Bank of England left its main interest rate at 0.25%. While this was no surprise, the rates are a historically new low level.

Having cut its rate from 0.5% to 0.25%, in a bid to maintain the stability of the UK’s banking system in the aftermath of Brexit, the August decision to cut bank rates was the first such move since March 2009. As a further rate cut was expected in some quarters no change was seen as a positive. At 9-0, the vote of MPC members, including the governor Mark Carney, was unanimous.The Bank continued to hint throughout September that it was likely to cut rates further, citing November economic forecasts being similar to those of August.

"A majority of members expected to support a further cut in bank rate to its effective lower bound at one of the MPC's forthcoming meetings during the course of the year," the Bank said in the minutes of its latest MPC meeting.

The damning verdict on Project Fear was issued 21 September by the Office for National Statistics. Government experts revealed that Cameron and Osborne’s dire predictions had failed to emerge and the UK remained strong.

The report pointed out that GDP estimates to be published in October would give a much clearer indication of the impact: "Nevertheless, there has been no sign of a major collapse in confidence and, within the data that is available, some indicators of strength." So while the UK economy has not fallen at the first fence, the longer-term effects remain to be seen.

As September neared a close, on 23rd Sept the pound struggled after British Foreign Secretary Boris Johnson said that negotiating a deal with Europe may not take two years. He added that the ‘divorce proceedings’ would likely begin early 2017.

Outlook

The GDP data for September was positive, but the pound remains weak overall. While it will be surprising if the Bank of England cuts rates further still, they have indicated that this is a distinct possibility.

The fear of Brexit fall-out and the timing or speed of when Article 50 will be invoked was the primary contributing factor to the pound’s summertime woes.

Moving forward, there are concerns about recent decisions regarding Deutsche Bank that will continue to impact euro-sterling rates. The health of the German lender is under scrutiny since the US Justice Department suggested it pay $14bn to settle a number of investigations related to mortgage securities.

This led to speculation over whether the German government would step in and support the ailing bank, whose potential downfall could have wider repercussions for the global banking system.

If, as indicated last week, Angela Merkel does not bail out Deutsche Bank, there will be a massive and far-reaching impact across Europe and beyond.

We would expect the repercussions of Deutsche Bank failing to be significant euro weakness. It is likely that fears of contagion and concerns regarding security of the markets and investments will grip the Eurozone resulting in further euro weakness.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Next Article: S1 Health Cover or French Pension?

Thank you for showing an interest in our News section.

Our News section is no longer being published although our catalogue of articles remains in place.

If you found our News useful, please have a look at France Insider, our subscription based News service with in-depth analysis, or our authoritative Guides to France.

If you require advice and assistance with the purchase of French property and moving to France, then take a look at the France Insider Property Clinic.