April was an interesting month for the pound to euro (GBP/EUR) exchange rate and it seems as if GBP/EUR found a new resistance level at the 1.20 mark, writes Ben Scott.

With the upcoming UK general election, there’s plenty of speculation as to whether the currency pair will breach that level in the next month.

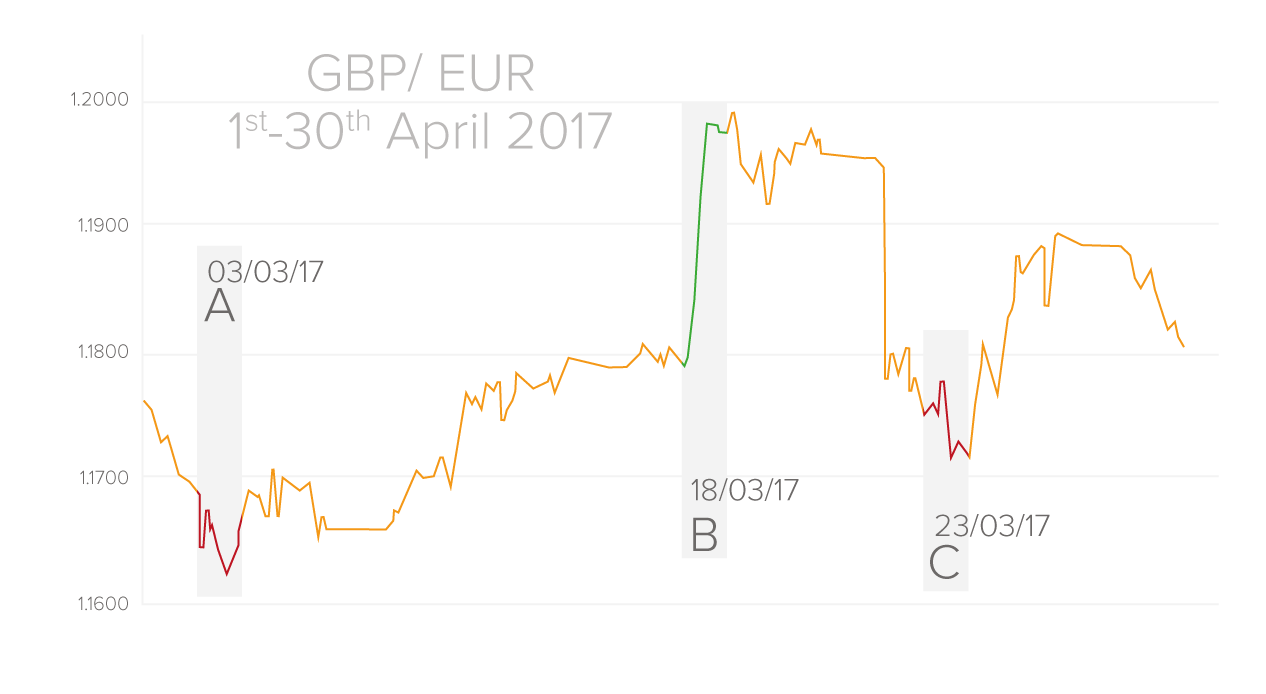

Towards the end of March, GBP/EUR was trending in the region of 1.15 and at the start of April picked up to 1.17 (point A). The currency pair reached 1.1990 – just a shade below the 1.20 threshold – at its pinnacle in the middle of the month.

April brought with it the announcement that French political front runners Emmanuel Macron and Marine Le Pen were through to the second round of voting on May 7th – no surprise as polls had forecast this result. However, the reliability of polls had been thrown into question following Brexit and Trump’s election win; polls had suggested Britain would remain and Trump would fall short of power.

At the start of May two candidates fought for the Presidency – Le Pen lost, allowing the European Union to breathe a sigh of relief as France will now remain in the eurozone. Had Le Pen won, the world may have witnessed the beginning of the disintegration of the currency bloc.

Meanwhile in Britain, April also saw Prime Minister Theresa May announce that UK voters would head to the polls once again for the second time in less than a year – this time to vote on the government. Sterling jumped (point B) significantly on the news.

There are several benefits to holding a snap election for May; with the labour party fractured and Jeremy Corbyn’s leadership skills debated by many, he could be a weaker opponent than a new leader, if he were to retire. A landslide win, as predicted by the polls, would give May her own mandate and more power in Brexit negotiations. Markets viewed the snap election announcement as pound positive as investors rushed to buy sterling. If the Tories do win in June, it’s likely the pound could rally significantly as markets anticipate a smoother Brexit process.

Another political factor to offer the GBP exchange rate a boost was the announcement by the EU Commissioner for Trade which plainly stated that she believed a deal would been made.

When asked if a free-trade agreement could be met, Cecilia Malmstrom commented: ‘It's uncharted territory but I'm sure we will solve it. We will have a free trade agreement, that is for sure.’

The optimism gave the pound a boost, but unfortunately for sterling, news reports of a ‘disastrous’ first meeting between Theresa May and President of the European Commission Jean-Claude Juncker who suggested ‘Brexit cannot be a success’, encouraged GBP to retreat.

Sterling is likely to be incredibly volatile amid Brexit negotiations and the run-up to the snap election. Although a Conservative victory is expected, the four-week run-up is plenty of time for views to change, meaning investors are likely to remain wary of the possibility of an unpredictable result.

Moreover, the pound fell against the euro (point C) on the news that Emmanuel Macron had won the first round of the French election, but the single currency failed to hold onto gains following the second round despite Macron reigning victorious. It appears as if a number of questions have been raised surrounding the future of France under Macron’s leadership which may continue to weigh on the euro.

The UK yielded disappointing first quarter growth figures in April; while the annual ecostat rose from 1.9% to 2.1% slightly below the 2.2% forecast, the quarter-on-quarter figure did the pound no favours when it came in at 0.3%, following the previous month’s 0.7%.

Since the referendum, living costs have increased as inflation rises and many industry experts believe that rising consumer prices could cause a significant squeeze on households, especially as wage growth rose at its slowest pace since 2014 according to the Office for National Statistics (ONS).

Senior ONS statistician David Freeman commented: ‘A joint record employment rate and a new record high for the number of vacancies point to continued strength in the labour market. However, higher inflation, coupled with subdued earnings increases, means that the real growth rate in pay has tailed off to just above zero.’

Additionally, Markit’s March purchasing managers’ indexes showed a slight slowing in both the manufacturing and construction sectors, but a small upswing in the services sector. UK industrial production fell far lower than economists had expected, coming in at 2.8% on the year, rather than growing from the previous 3.3% to 3.7% as expected.

On a positive note, the UK’s trade deficit shrank to the lowest level since before the Global Financial Crisis (GFC). The UK government borrowed £52bn in the last financial year, noting a fall of £20bn in comparison to the previous year. The deficit is slowly improving following the massive £151.7bn that was recorded in 2009-2010 following the height of the GFC.

Additionally, UK Confederation of British Industry (CBI) retail sales data outperformed predictions and quelled fears that the UK is experiencing a Brexit catalysed consumer-led slowdown.

Economic Data to Impact EUR

Meanwhile in the Eurozone, European Central Bank (ECB) President Mario Draghi caused euro fluctuations throughout the month. On the 27th April, the single currency was able to jump higher on comments from the experienced central banker as he noted the eurozone recovery was becoming ‘increasingly solid’. Eurozone PMI’s released in recent months have shown productivity returning to its healthiest levels since 2011.

Draghi commented: ‘Incoming data—notably survey results—bolster our confidence that the ongoing economic expansion will continue to firm and broaden.’

Earlier in the month Draghi spooked markets when he commented that he had no plans to increase interest rates any time soon. The central banker suggested that the current negative rate is accommodative for the ongoing recovery.

German inflation hit 2.0% in April on the year from the previous month’s 1.6%, jumping past the 1.9% forecast. Meanwhile, Eurozone inflation also rose to reside at 1.9% YoY.

US Dollar Weakness

Markets saw a change of pace in April with the mighty US dollar falling lower against other currency majors. The euro managed to record a five-and-a-half month high versus the buck trading at levels of 1.0935, while the pound managed to attain a seven-month high trending in the region of 1.2970.

A large part of the US dollar’s weakness was attributed to several poor data releases and the failure of President Trump’s reforms to be put in place, bringing into question the effectiveness of the administration.

GBP/EUR Forecast

The short-term forecast for GBP/EUR is likely to be dominated by how political events unravel. It’s expected that economic data will take a back seat as markets digest the French election result, UK election, and ongoing Brexit negotiations. Once the fallout from the UK general election has settled, economic data is likely to be more influential once the political landscape has stabilised; however, Brexit will still play a large part in GBP movement over the next two years.

Additionally, investors will be waiting for central banks to blink and tighten monetary policy. Markets are keenly anticipating the prospect of Bank of England (BoE) interest rate increases at some point in the future, if inflation continues to bite. Additionally, Draghi’s speeches are likely to cause market movement as investors look for clues of when the ECB will begin to tighten policy in line with calls from nations such as Germany.

Labour market, inflation, and gross domestic product (GDP) numbers are therefore likely to be extremely influential in coming months as these are some of the key factors central banks assess before adjusting monetary policy.

Ben Scott

Foreign Exchange Ltd

www.fcexchange.co.uk

Related Reading: